Flight cancellations are no longer rare inconveniences—in 2025, they’re part of the travel reality in the U.S. Whether due to severe weather, staffing shortages, or mechanical issues, thousands of flights are disrupted daily.

That’s why having the best travel insurance for flight cancellations can save you from unexpected costs, long airport waits, and rebooking chaos. In this guide, we’ll cover what to look for, top providers, and expert tips to help you choose the right plan. Whether you’re flying for business or vacation, having solid travel insurance for flight cancellations makes a huge difference.

If you want a complete overview of what travel insurance typically covers—including medical, baggage, and interruption protection—check out our full guide here: What is Travel Insurance?

1. Why You Need Travel Insurance for Cancelled Flights

\ven a minor delay can lead to big expenses—meals, hotels, ground transport, or booking a new flight yourself. Without insurance, these costs come out of pocket. Some travelers have even reported spending over $1,000 on unexpected overnight stays or last-minute rebookings when their flights were suddenly cancelled.

That’s where travel insurance for flight cancellations becomes essential. Not only does it reimburse you for covered costs, but it also gives you peace of mind. Delays, missed connections, or last-minute itinerary changes are much easier to manage when you’re backed by travel insurance for flight cancellations.

✅ What a good policy typically covers:

Trip cancellation due to illness, weather, or emergencies

Trip interruption after you’ve already departed

Flight delay benefits (hotel + meals)

24/7 emergency travel assistance

“Cancel for Any Reason” (CFAR) upgrade options

📌 Tip: Peak season, winter weather, and budget airlines increase the risk of cancellations. Choose a plan that includes broad disruption coverage.

2. Top U.S. Travel Insurance Providers in 2025

Here’s a breakdown of leading insurance companies offering strong cancellation benefits:

Provider

Best For

Notable Feature

Allianz Travel

Business & frequent flyers

Fast claims + strong trip interruption coverage

Travel Guard

Customizable plans

Covers delays, cancellations, medical

AXA Assistance USA

Budget-conscious travelers

COVID-related cancellation included

Generali Global Assistance

Full-service support

24/7 concierge + robust delay coverage

Berkshire Hathaway Travel Protection

High-end coverage

Includes CFAR + delay reimbursement

🎯 Pro Tip: Many basic plans only reimburse delays after 12+ hours. Look for policies that kick in after 3–6 hours for better protection.

When selecting travel insurance for flight cancellations, it’s important to look beyond brand names. Read reviews, compare policy terms, and focus on delay reimbursement timing. Every hour counts when you’re stuck at an airport.

3. Key Features to Compare

3. Key Features to Compare

When evaluating travel insurance for flight cancellations, it’s crucial to go beyond price tags and compare the actual protection you’re getting. Here are the five most important features you must look for—and why they matter when your trip gets disrupted:

🛫 Trip Cancellation Limit

This determines the maximum amount your policy will reimburse if you cancel your trip for a covered reason before departure.

Why It Matters: Your travel insurance for flight cancellations should always cover 100% of your prepaid, non-refundable expenses—including flights, hotels, tours, and even prepaid event tickets.

✅ Look for policies with cancellation limits equal to or greater than your total trip cost.

🔁 Trip Interruption Coverage

This protects you after your trip has already started—if you need to return early or miss parts of your itinerary.

Why It Matters: A strong travel insurance for flight cancellations plan will refund the unused portion of your bookings, plus additional expenses like a new return flight.

✅ Useful for emergencies like family illness, natural disasters, or civil unrest at your destination.

⏱️ Flight Delay Benefits

This covers costs if your flight is significantly delayed due to weather, mechanical failure, or other covered reasons.

Why It Matters: Many travelers spend hundreds on last-minute hotel rooms, food, or transportation during delays.

✅ Choose travel insurance for flight cancellations that provides delay compensation after 3–6 hours, not 12+ hours like many basic plans.

❎ CFAR (Cancel For Any Reason) Option

This optional upgrade lets you cancel your trip for literally any reason, even if it’s not listed in the policy’s covered reasons.

Why It Matters: Life is unpredictable. CFAR gives you up to 75% reimbursement even if you cancel because of personal anxiety, job obligations, or just a change of heart.

✅ Most travel insurance for flight cancellations plans require CFAR to be purchased within 10–21 days of your initial booking.

📞 24/7 Customer Service and Claims Support

Disruptions often happen outside business hours—and having live support is essential.

✅ Only choose travel insurance for flight cancellations providers with 24/7 multilingual support lines and fast claims processing.

Why It Matters: Whether you’re stuck overnight in an airport or stranded abroad, being able to call a real human for help with rebooking, claims, or medical assistance makes all the difference.

4. Where to Buy Travel Insurance for Flight Cancellations

You can compare quotes and filter by features on these platforms:

Squaremouth — Filter by delay time, CFAR, and provider reviews

InsureMyTrip — Includes “Best for Delays” tags + verified ratings

Provider websites — May offer lower prices or extra perks for direct bookings

🔹 Always read the fine print: some policies only cover cancellations for “covered reasons” unless you opt into CFAR.

Using these platforms makes it easier to find travel insurance for flight cancellations that fits your trip. Whether you’re taking a short domestic flight or a cross-country adventure, protection matters.

✅ Quick Comparison Table

Provider

Best For

Cancellation Coverage

Allianz

Frequent flyers

✅ Up to 100% of trip cost

Travel Guard

Custom plans

✅ CFAR optional

AXA

Budget option

✅ Fixed limits

Generali

Full-service support

✅ Concierge + delay perks

Berkshire Hathaway

Premium travelers

✅ Best CFAR benefits

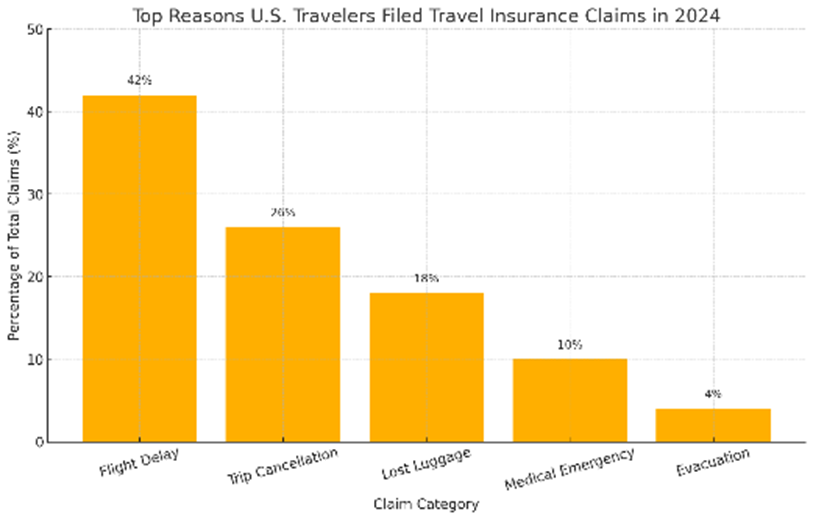

5. Chart: Top Reasons Travelers Filed Claims in 2024

Wondering what goes wrong most often when people travel? Just look at this breakdown it says it all.

As shown, flight delays accounted for 42% of all claims, making them the single most common disruption. Trip cancellations followed at 26%, often due to weather, illness, or airline system failures. Lost or delayed baggage was the next most frequent reason at 18%, a risk especially common at major international hubs.

Less frequent but still significant were medical emergencies (10%), highlighting the need for coverage even on domestic trips, and emergency evacuations (4%), which, while rare, carry extremely high costs when they occur.

📊 This chart clearly shows that delays and cancellations make up nearly 70% of travel insurance claims. Planning for those risks is no longer optional. Choosing travel insurance for flight cancellations with solid delay and interruption terms is critical for frequent travelers.

6. How to Choose the Right Travel Insurance for Flight Cancellations

The cheapest plan isn’t always the best. What matters is finding coverage that actually fits how you travel—and how flexible you need to be.

Here’s a step-by-step checklist to help you compare and choose wisely:

✅ Step 1: Assess Your Risk Profile

Ask yourself:

Are you flying during peak seasons (winter holidays, summer weekends)?

Are you flying budget carriers or airlines with frequent cancellations?

Is your trip non-refundable (hotels, tours, flights)?

Do you have pre-existing health concerns or dependents?

If you answer “yes” to most of these, you need stronger trip cancellation and delay coverage—possibly with CFAR (Cancel For Any Reason).

✅ Step 2: Compare These Key Features Side-by-Side

Feature

What to Look For

Why It Matters

Trip Cancellation Limit

At least equal to total prepaid trip cost

Ensures you’re fully reimbursed

Trip Interruption

Return flight + unused booking value

Helps if return trip is cut short

Flight Delay Coverage

Starts at 3–6 hours, not 12+

Reduces hotel/meal out-of-pocket costs

CFAR Option

50–75% refund flexibility

Adds coverage for personal or unexpected reasons

Emergency Support

24/7 live help with rebooking or claims

Critical during time-sensitive disruptions

✅ Step 3: Read Real Customer Reviews

Don’t just compare features—compare claim success stories and complaints. Did the provider delay payment? Deny claims unfairly? Have poor customer support?

Delay coverage window (e.g., 3+ hours vs 12+ hours)

Provider reputation scores

CFAR availability

Medical + baggage inclusion

Many travelers miss out on better options because they buy directly through the airline or booking site, which often offers limited protection. Comparing your options ahead of time ensures that your travel insurance for flight cancellations is tailored not just convenient.

7. What’s Not Covered in Most Cancellation Policies?

Even with a solid policy, not everything is reimbursable. Understanding the exclusions in travel insurance for flight cancellations is essential if you want to avoid unpleasant surprises during claims.

Here are the most common limitations travelers should know:

❌ 1. “Known Events” or Foreseen Disruptions

If a snowstorm is already named, a union strike is in the news, or a government advisory is issued before you buy your policy—you’re not covered.

Example: Buying a plan after a hurricane warning is issued for your destination? That’s considered a “known event,” and most insurers won’t reimburse you for canceling.

📌 Tip: Always purchase your travel insurance for flight cancellations as soon as you book your trip to avoid missing protection for future disruptions.

❌ 2. Canceling for Personal Reasons

Most policies don’t cover cancellations because:

You changed your mind

The weather looks bad, but the flight isn’t canceled

You found a cheaper option later

Unless you have CFAR (Cancel for Any Reason) coverage, these situations are excluded.

📎 CFAR gives you added freedom—but it must be purchased early and usually only reimburses 50–75% of your trip cost.

❌ 3. Pre-Existing Medical Conditions (Without Waiver)

If you cancel due to a medical condition you had before booking, your claim may be denied—unless:

You bought the policy within 10–21 days of your first trip payment

You added a pre-existing condition waiver

Without this, even legitimate health-related cancellations may not be honored by your travel insurance for flight cancellations provider.

❌ 4. Entry Denials and Documentation Issues

Insurance generally doesn’t cover:

Visa denials

Missing passports

Invalid COVID-19 certificates

Refused entry at customs or immigration

It’s the traveler’s responsibility to meet all destination entry requirements. These administrative issues are not covered reasons for trip cancellation.

❌ 5. Not Accepting the Airline’s Rebooking Offer

Here’s a common but costly mistake: your airline cancels your flight and offers a new one, but you book your own alternate flight instead—without insurer approval.

If you do this, your reimbursement claim may be denied because you didn’t accept the official resolution or failed to follow the process.

🛑 Always contact your insurer first if you’re considering alternate arrangements. Many travel insurance for flight cancellations policies require pre-approval for claims.

📌 Final Pro Tip

Before buying, carefully review the policy’s “General Exclusions” section. If anything seems vague or confusing, don’t hesitate to call the insurer and ask:

“Would this situation be covered under your cancellation policy?”

It’s better to ask a hypothetical than lose real money later.

8. How Much Does Travel Insurance for Flight Cancellations Cost?

The price of travel insurance for flight cancellations isn’t fixed—it depends on multiple factors unique to each traveler. Here’s a detailed breakdown of the main cost drivers:

🔍 1. Your Age

Insurance providers use age as a key risk indicator. Older travelers are statistically more likely to cancel due to illness, injury, or medical conditions. As a result:

A 30-year-old may pay $50–$80 for a basic plan

A 65-year-old could pay over $250 for similar coverage

Tip: Some providers offer family bundles or child discounts, so check if younger dependents are included free or at reduced rates.

💵 2. Total Trip Cost

Your insurance premium is usually calculated as a percentage of the total non-refundable prepaid expenses—typically between 4% and 10%. So:

For a $1,500 trip, expect $60–$100 in premium

For a $5,000 trip, premiums rise to $200–$400

More expensive trips require more coverage, especially if hotel, airfare, and activities are prepaid and non-refundable.

3. Coverage Type & Benefit Limits

Basic plans cover cancellation for specific reasons (illness, weather, etc.) and are cheaper

Comprehensive plans include trip interruption, flight delays, baggage protection, and more

Higher benefit limits (e.g., $100,000 trip interruption vs $25,000) mean higher premiums

When selecting travel insurance for flight cancellations, always balance benefit levels with your trip value. Overpaying for $100,000 coverage on a $2,000 trip isn’t efficient—but underinsuring can leave you exposed.

4. CFAR Inclusion (Cancel for Any Reason)

CFAR is an optional upgrade that allows you to cancel for any reason not otherwise covered, like:

Sudden work conflicts

Nervousness about weather or COVID rates

Simply changing your mind

But this flexibility comes at a cost:

Adds 40%–70% to your base premium

Typically reimburses only 50–75% of trip cost

Must be purchased within 10–21 days of booking

You must cancel at least 48 hours before departure

📊 Example Comparison Table

Trip Cost

Traveler Age

CFAR Included?

Estimated Premium Range

$1,500

30

❌ No

$50 – $80

$1,500

30

✅ Yes

$80 – $120

$3,000

45

❌ No

$90 – $130

$3,000

45

✅ Yes

$140 – $200

$5,000

65

✅ Yes

$250 – $350

🧠 Key Takeaway

If your trip is relatively low-cost and your travel plans are firm, a basic travel insurance for flight cancellations plan is likely sufficient.

For high-value trips, peak season bookings, or uncertain schedules, CFAR is well worth the extra premium.

Even though adding CFAR raises the premium, it could save thousands in non-refundable expenses if plans change unexpectedly.

Final tip: Always get quotes from 2–3 comparison platforms, and run cost estimates both with and without CFAR to see which gives you the best mix of cost and peace of mind.

9. Real Cost Scenario: Solo Traveler vs Family of Four

Here’s a deeper look at two real-world examples to help you understand how pricing works when choosing travel insurance for flight cancellations in the U.S.

🧍 Case 1: Solo Traveler Booking a City Trip

Traveler Profile: 28-year-old freelance designer

Departure: Denver

Destination: New York City

Trip Duration: 5 days

Total Trip Cost: $1,200 (roundtrip airfare + boutique hotel + concert ticket)

Insurance Comparison:

Coverage Type

Premium

What It Includes

Basic Plan

$65

Covers trip cancellation, delay after 6 hours, trip interruption, and baggage loss

With CFAR Upgrade

$102

All of the above + Cancel for Any Reason (up to 75% refund if canceled for a non-covered reason)

💡 Insight: For short domestic trips like this, travel insurance for flight cancellations may seem optional—but if you’re attending an event or staying in non-refundable lodging, a basic plan is a low-cost safety net. And CFAR ensures flexibility if, say, a freelance client books a last-minute gig and you need to cancel.

👨👩👧👦 Case 2: Family Vacation with Major Prepaid Costs

Traveler Profile: Married couple with two children (ages 7 and 10)

Departure: Orlando

Destination: San Francisco

Trip Duration: 7 days

Total Trip Cost: $4,800

Flights: $1,600

Hotel: $2,000

Theme park and tour bookings: $1,200

Insurance Comparison:

Coverage Type

Premium

What It Includes

Standard Cancellation Plan

$220

Protects all prepaid trip costs from cancellation or delay (after 12 hours), trip interruption, baggage loss

CFAR-Inclusive Plan

$360

Includes all standard protections + allows cancellation for any reason up to 48 hours before departure (75% reimbursement)

📌 Scenario Insight: With two kids, anything can happen—illness, school event changes, unexpected family emergencies. In this case, investing in travel insurance for flight cancellations with CFAR gives the family peace of mind that they won’t lose thousands if they need to back out for any reason.

👉 Takeaway: Why These Plans Matter

For solo travelers, a basic policy is very affordable and sufficient for most domestic flights.

For families or high-cost vacations, it’s smart to pay slightly more for CFAR—especially when prepaid bookings are non-refundable.

In both cases, the cost of travel insurance for flight cancellations is only 2%–7% of the total trip cost—but can prevent 100% loss in the event of disruption.

🧠 Pro Tip: Always align your coverage with your trip value, family situation, and personal flexibility. A $300 policy may seem expensive—until it saves you $3,000.

👨👩👧👦 Case 3, One Delay, Four Thousand Dollars

Let’s take a real-world example.

In December 2024, a couple from Denver was flying to New York for their anniversary trip. Their flight was cancelled just two hours before departure due to unexpected snowstorms. The airline offered to rebook—but the next flight was two days later. They had already prepaid for a Manhattan hotel, Broadway tickets, and a river cruise.

With no insurance, they would have lost:

$620 in hotel fees (non-refundable)

$400 in show tickets

$110 in transportation bookings

$1,200 in new airfare they had to purchase last-minute from another airline

Thankfully, they had a travel insurance policy that included trip cancellation, delay reimbursement, and interruption benefits. Their total reimbursement? $3,850. It didn’t make up for the stress, but it saved them from losing their entire travel budget.

And this is just one story. Thousands of Americans travel every week without realizing how vulnerable they are to cancellation-related expenses. Whether it’s a missed connection due to a delay or a weather-induced cancellation, the lack of coverage can turn a fun trip into a financial loss. Instead of losing your trip—and your money—you gain a safety net that helps you recover fast.

🙋 Frequently Asked Questions (FAQ)

Q1. Can I buy travel insurance for flight cancellations after I’ve already booked my flight?

A: Yes—but the sooner, the better. Most providers allow purchase up until the day before departure. However, to be eligible for full benefits (like CFAR or pre-existing condition waivers), you often need to buy the policy within 10–21 days of your initial trip payment.

Q2. What if the airline already refunds me—can I still file a claim?

A: No. Travel insurance for flight cancellations only reimburses non-refundable losses. If your airline provides a full refund or rebooks you for free, you cannot “double dip” and claim that cost from the insurer.

Q3. Does travel insurance for flight cancellations work for domestic U.S. flights?

A: Absolutely. Even for domestic flights, cancellation insurance covers hotel bookings, tours, transit, and non-refundable event tickets. It’s especially helpful if you booked multiple services separately (e.g., hotel via Expedia, show tickets, etc.) rather than through a travel package.

Q4. What’s the difference between “trip interruption” and “trip cancellation”?

A:

Trip cancellation covers pre-departure scenarios (e.g., your trip is cancelled before it starts).

Trip interruption applies after departure—you’re mid-trip and need to return early or miss part of your itinerary. Both are critical components of comprehensive travel insurance for flight cancellations.

Q5. Can I cancel for work-related reasons?

A: Usually not—unless it’s listed as a “covered reason” or you have CFAR. Most standard policies exclude cancellations due to employer changes, unless you’re in the military or had pre-approval from the insurer.

Final Thoughts

Flying in 2025 means expecting the unexpected. From airline strikes to bad weather, cancellations are part of the deal. But with the right travel insurance for flight cancellations, you can turn chaos into a manageable inconvenience.

Don’t leave your trip to chance. Take time to compare plans, check the delay and cancellation terms, and consider CFAR if you need maximum flexibility. You can’t stop your flight from being cancelled—but you can make sure it doesn’t ruin your travel plans. With the right travel insurance for flight cancellations, you won’t just save money you’ll save your entire trip from falling apart.

About Us

Trip & Save helps American travelers prepare for unpredictable journeys with insurance-backed peace of mind. We review the best plans so you can focus on the experience not the what ifs.

")

")

")

")