Disclaimer: This article is for educational purposes only. Health insurance coverage varies depending on providers, visa type, and travel duration. Always verify with your insurer before departure.

South Koreans traveling to the U.S. for leisure, study, or business face one of the most expensive healthcare systems in the world. A simple ER visit can cost thousands of dollars, and without adequate travel insurance, even minor issues can lead to overwhelming debt.

This guide explains why South Korea to U.S. travel insurance is essential in 2025, how to choose the right policy, and which insurers offer the best protection. We also include real case studies, FAQs, and what coverage is required for visa holders.

1. Why You Need South Korea to U.S. Travel Insurance

The U.S. does not offer free or subsidized healthcare for foreign travelers. A broken arm can cost $3,000–$5,000. An ambulance ride? $1,200 or more. Without coverage, travelers are 100% liable.

South Korea to U.S. travel insurance covers:

Emergency medical treatment (recommended minimum: $100,000)

Emergency evacuation and repatriation

Hospitalization and surgeries

COVID-19 treatment and testing (if specified)

Trip delays, cancellations, or interruptions

Lost or delayed baggage

Dental emergencies

24/7 multilingual support

💡 Even if you have Korean National Health Insurance, it does not cover medical care received in the U.S.

2. What Coverage Should You Look For in South Korea to U.S. Travel Insurance?

When choosing South Korea to U.S. travel insurance, you need more than just the basics. The U.S. has the world’s most expensive healthcare system, and even minor accidents can cost thousands.

✅ Essential Coverage Checklist:

Emergency medical expenses (minimum $100,000) – Anything less will leave you exposed

Hospitalization & surgery – Includes ICU, emergency room, and specialist care

Emergency evacuation – Air ambulance or ground transport for critical care

Repatriation of remains – Required by most U.S. visa programs

Prescription medication – Out-of-pocket drug costs are high in the U.S.

Trip cancellation & interruption – Refunds for non-refundable bookings

Rental car damage waiver – Optional but smart if you plan to drive

🩹 Optional Riders:

COVID-19 treatment and quarantine

Dental emergencies

Business travel disruption

Sports & activity injury (especially important for skiing, hiking, or surfing)

If your plan doesn’t offer these, it’s not real South Korea to U.S. travel insurance—it’s just a false sense of security.

3. Real Case: Covered vs. Uncovered Scenarios

Case 1 – No Insurance, Major Cost:

Minji L., a Korean university student visiting New York on a short visa, slipped on an icy sidewalk and dislocated her shoulder. Without South Korea to U.S. travel insurance, she was billed:

$9,800 for emergency room treatment

$4,500 for imaging and orthopedist consultation

$1,100 for prescription medication and two follow-up visits

Her Korean health insurance covered none of it. She ended up borrowing from her family to avoid collections.

Case 2 – Fully Insured and Hassle-Free:

Mr. and Mrs. Park, retired travelers from Busan, purchased a comprehensive South Korea to U.S. travel insurance plan with Hanwha before flying to Los Angeles. Mrs. Park developed a high fever and was admitted to a local hospital.

Thanks to their insurance:

The hospital accepted direct billing

All treatment and medication were covered 100%

The insurer rebooked their flights at no cost

Mr. Park later said, “The peace of mind was priceless. We were able to focus on her recovery, not the bill.”

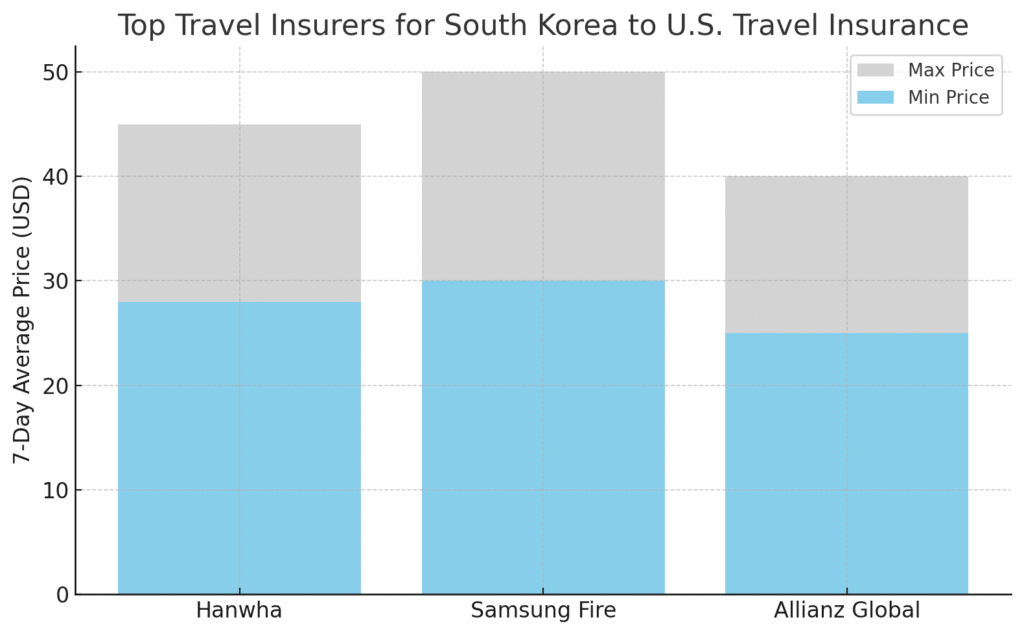

4. 🏆 Best Travel Insurers for South Koreans Visiting the U.S.

Here’s a closer look at the top providers offering South Korea to U.S. travel insurance:

Insurer

Key Benefits

Avg. Price (7 Days)

Hanwha

Korean-English support, partnerships with major U.S. hospitals

$28–$45

Samsung Fire

Strong international hospital network, COVID coverage included

$30–$50

Allianz Global

24/7 multilingual call center, fast claim processing via app

$25–$40

Pros & Cons Summary:

Hanwha: Best for older travelers and those needing Korean-speaking assistance. Limited mobile tools.

Samsung Fire: Great for family plans, strong global reputation. Slightly pricier.

Allianz: Best app and online tools, but may lack Korean-specific support.

Each of these companies offers South Korea to U.S. travel insurance plans that meet or exceed U.S. immigration and travel protection standards.

This chart highlights the typical South Korea to U.S. travel insurance costs from three major insurers. Allianz offers the most affordable entry point, starting around $25, while Samsung Fire provides broader coverage with prices up to $50. Hanwha offers bilingual support and strong U.S. partnerships, with midrange pricing between $28 and $45.

5. Credit Card Insurance vs. Dedicated Travel Policies

Many Koreans believe their credit card covers enough. Reality: most card plans are not suitable substitutes for true South Korea to U.S. travel insurance.

Common Gaps in Credit Card Insurance:

Max coverage usually $10,000–$25,000

Emergency evacuation not included

No repatriation services

Coverage limited to 7–15 days

Age exclusions for seniors (typically 70+)

💡 Unless your credit card clearly offers $100,000+ coverage with evacuation and English documentation, you still need standalone South Korea to U.S. travel insurance.

6. Family Coverage & Group Discounts (Expanded)

If you’re traveling with loved ones, bundling your South Korea to U.S. travel insurance into a family or group plan can save money and reduce paperwork. Most major insurers in both South Korea and the U.S. offer multi-traveler discounts, especially if you’re on the same itinerary.

Benefits of Family Plans

Feature

Description

Family Discounts

Most insurers offer 10% to 20% discounts for two or more travelers under the same policy.

Children Coverage

Kids under 18 (or 21 for full-time students) are often included at reduced rates or for free.

One Policy, One Claim Process

Less hassle in emergencies—only one certificate to carry, one provider to contact.

Add-ons for Maternity & Sports

Some South Korea to U.S. travel insurance policies allow pregnancy coverage, sport injury protection, and childcare assistance if parents are hospitalized.

This is especially valuable if you’re traveling with:

Infants or toddlers

Teenagers with known medical needs

Elderly parents with pre-existing conditions

💡 Pro Tip: Many Korean insurers like Hanwha or Samsung Fire let you customize group plans online before you fly.

What to Check Before Buying a Family Plan

Before buying any South Korea to U.S. travel insurance plan for your group, ask these questions:

Are dependents automatically included, or do you need to list them individually?

Are there age-based rate increases, especially for seniors over 65 or infants under 1?

Does the discount apply after two people, or do you need three or more travelers?

Can you add maternity or injury coverage if you’re traveling with pregnant family members or planning active adventures?

✈️ For long trips or multiple U.S. destinations, a bundled South Korea to U.S. travel insurance plan provides not only cost savings—but peace of mind for the entire family.

7. Mistakes to Avoid When Choosing South Korea to U.S. Travel Insurance (Expanded)

Even smart travelers can make costly mistakes when purchasing travel insurance. The U.S. healthcare system is complex, and misunderstanding your policy can lead to unexpected bills or denied claims. Below are the most common pitfalls Koreans fall into—and how to avoid them.

❌ Common Mistakes Koreans Make

Assuming Korean National Health Insurance Covers the U.S.

It doesn’t. The Korean NHIS only reimburses for pre-approved overseas treatments, and even then, coverage is minimal.

South Korea to U.S. travel insurance is required for any real protection abroad.

Skipping Evacuation and Repatriation Coverage

A medical evacuation in the U.S. can cost over $100,000.

Repatriation (return of remains or critical care transport) is a mandatory clause for most visa categories like J1, F1, and work exchanges.

Not Disclosing Pre-Existing Conditions

If you had asthma, diabetes, or a recent surgery and didn’t declare it, your South Korea to U.S. travel insurance provider may deny your claim entirely.

Many insurers offer add-ons or waivers—but only if declared at sign-up.

Relying Too Much on Credit Card Travel Insurance

Most Korean credit cards only provide $10,000–$25,000 in medical coverage, often excluding evacuation, ICU, or pre-existing illness care.

These plans also often lack English documentation, which is required by U.S. hospitals and customs officials.

Not Getting the Policy in English

U.S. immigration and medical staff cannot verify Korean-only policies.

Your South Korea to U.S. travel insurance must have an English-language certificate and benefits summary to be valid for visa processing and treatment access.

🔎 Final Reminder

South Korea to U.S. travel insurance is not just a checkbox—it’s a lifesaver when things go wrong abroad. By avoiding these five common mistakes, you can travel with confidence, knowing you’re truly protected.

8. When Is Insurance Required for U.S. Entry?

For some categories of travelers, South Korea to U.S. travel insurance is not optional:

You must show proof of insurance if you are:

A J1 or F1 visa holder (students, researchers, interns)

Applying for Humanitarian parole

A short-term exchange visitor on a special work-study program

Minimum U.S. entry requirements:

$100,000 emergency medical coverage

Medical evacuation and repatriation of remains

English-language proof of insurance (hard copy or PDF)

Failure to show proof can result in visa rejection or customs delays.

9. How to Use South Korea to U.S. Travel Insurance in Real Emergencies

South Korea to U.S. travel insurance isn’t just about buying the policy—it’s about knowing how to use it in an emergency. Whether it’s a minor illness or a serious accident, here’s what to do step-by-step:

1. What to Do If You Need Medical Help

Call your travel insurance provider using the emergency number printed on your certificate.

Request an in-network hospital or clinic. Your South Korea to U.S. travel insurance may not fully reimburse you if you go out-of-network.

Show your Certificate of Insurance at check-in. This proves you have active South Korea to U.S. travel insurance.

If direct billing isn’t available, pay upfront and keep all receipts.

File a claim online or through the mobile app within the time window (often 48–72 hours).

💡 Most travelers don’t realize that not calling the insurer first can reduce reimbursement or void the claim. Always contact your provider before or immediately after seeking treatment.

2. What Documents Do You Need?

Hospitals in the U.S. may deny non-emergency treatment unless you show valid South Korea to U.S. travel insurance documents:

Must-Have Document

Why It Matters

Insurance Certificate (English)

Proof of coverage and identity

Policy Number & Valid Dates

Verifies you’re currently insured

Emergency Contact Number

For billing and coordination

Itemized Receipts

Needed for reimbursement

Medical Records (if applicable)

For longer treatments or claims

🔍 Tip: Print a physical copy and email a digital version to yourself before leaving South Korea.

3. Real Case: Trouble Without a Printed Policy

Eunji K., a tourist from Busan, had stomach pain in San Francisco. She went to urgent care, but the clinic refused treatment without seeing her South Korea to U.S. travel insurance certificate. Since she didn’t have it printed or accessible, she was forced to go to the ER and paid over $2,000 out of pocket. Her claim was later partially denied for lack of insurer notice.

✅ Always print your documents and install the insurer’s mobile app before departure.

If you’re traveling with South Korea to U.S. travel insurance, keep both U.S. and Korean contacts accessible at all times. In a crisis, quick access can save time, money, and even lives.

10. FAQs

Q: Can I use Korean NHIS in the U.S.? A: No. It does not apply to treatment received abroad.

Q: Is COVID-19 covered? A: Most new travel policies include it, but confirm with your provider.

Q: Can I purchase after landing? A: Some plans allow this, but it’s always safer to buy before departure.

Q: Do I need insurance if I’m only staying for 5 days? A: Yes. Emergencies don’t check your calendar.

🧳 Final Thoughts

Traveling from South Korea to the U.S. is exciting—but also comes with significant financial and medical risks if you’re uninsured. In America, even a short ER visit can cost thousands of dollars, and emergency evacuations may exceed $100,000. For just $30 to $50, a proper South Korea to U.S. travel insurance plan can shield you from devastating bills and help you access top-tier care without hesitation.

Don’t assume your Korean health insurance or credit card coverage will be enough. Many travelers learn the hard way that these fall short in critical situations. Instead, take a few minutes to compare reputable insurers, understand the terms, and choose a plan that matches your age, trip duration, and specific needs like pre-existing conditions or family travel.

Insurance is more than a policy—it’s peace of mind. Travel smart. Travel safe. And give yourself the freedom to fully enjoy your journey in the U.S.

🌐 About Us

At Trip & Save, we specialize in simplifying travel insurance for global travelers. Whether you’re a student, retiree, business traveler, or family planning your first trip abroad, we bring you:

📝 Clear comparisons of top insurance providers

💡 Expert advice tailored to your destination

✅ Up-to-date guides on visa rules, entry requirements, and coverage must-haves

Our mission is simple: help you travel protected—without the stress or fine print confusion. Every article is built from expert insights, updated research, and real-world experience to help you make the best insurance choice possible.

")

")

")